NBFC Registration in India: Check Process, Cost, Eligibility, and Requirements

What is NBFC in Simple Terms?

A Non-Banking Financial Company (NBFC) is akin to a banking company and engaged in the business of providing loans, accepting deposits (only certain NBFCs), leasing, hire purchase, acquisition of stocks, insurance, etc.

What is the Meaning of NBFC Registration RBI?

In accordance with the RBI Act of 1934, supervises the process by which companies are registered under the Companies Act. The NBFCs play a vital role in the Indian economy. They facilitate financial operations, and they fill in for traditional banks when they are unable to extend loans or advances.

Moreover, the majority of deposits are accepted by non-banking finance corporations (NBFCs) according to prescribed schemes and agreements. Depositors can choose to pay in one lump sum or in instalments.

The RBI regulates and supervises the NBFCs in accordance to the RBI Act of 1934. According to Section 45-IA of the RBI Act, an NBFC cannot start or continue business in India without a NBFC registration certificate.

In India, the RBI is the only authority that can issue NBFC certificates. In recent years, RBI has simplified policies and regulations for the NBFCs. This makes the process easier to obtain a registration certificate.

Synopsis of the NBFC in India

NBFCs, or Non-Banking Financial Companies, are corporate entities registered under the Companies Act 2013 regulations. The Reserve Bank of India is responsible for regulating NBFCs.

NBFCs are still involved in providing services such as loans and advances, and acquiring shares, equities and debts issued either by the local or national government. Further, NBFCs differ from commercial banks and cooperative banks.

What are the Advantages of NBFC Registration in India?

- Save time and money: - Unlike traditional banks NBFCs can register instantly and quickly. A traditional bank license requires less time and cost.

- Easy Recovery of Loans: - NBFC banks are now able to recover their loans quickly through legal actions such as asset attachment, foreclosure or repossession.

- Industry growth ratio: - Despite recent significant changes, it is expected that the NBFC Banking Sector in India will maintain a Compound annual Growth Rate (CAGR), of 18.5% from 2021 to 2026.

- Easy Registration: - NBFCs are primarily focused on small borrowers, so obtaining a NBFC registration will be easier than registering as a bank.

What are the Requirements for NBFC License in India?

According to Section 45-IA in the RBI Act, 1934, a company wishing to register as an NBFC must meet the following requirements:

- Registration: - A company must be registered in order to apply for NBFC registration. This is per Section 3 of Companies Act 2013.

- Director Qualifications: - A third of the directors must have experience in finance.

- Unique business plan: - A comprehensive business plan describing the company's strategy for the next five years is required.

- Net Owned Fund (NOF): - If you are searching for "What is the minimum net owned Funds required by NBFCs for registration with RBIA" then let us tell you it will be minimum of Rs. 10 crores.

- Clear Credit History: – A company's CIBIL history must be clean.

- FEMA Compliant: - NBFCs that engage in foreign investment are required to comply with FEMA.

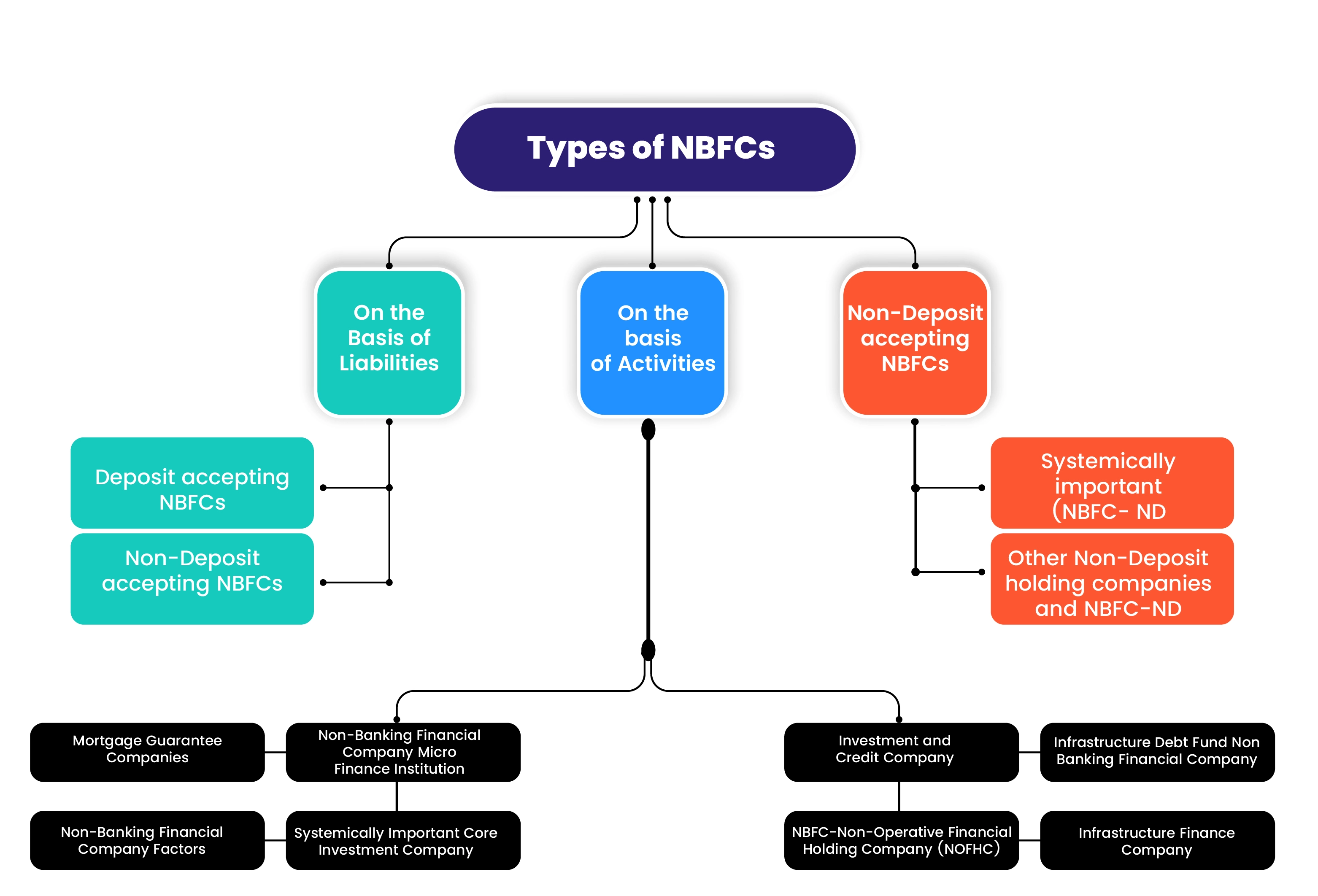

What are the Different Types of NBFCs in India?

Activities Not Classified as NBFC

The following activities are not considered NBFCs in India.

- Agriculture is a growing industry.

- Purchase and sale of any goods

- Industrial Activity

- Purchase/sale/Construction of a movable property

What is the Difference Between NBFCs and Banks?

|

Criteria for Comparison |

Non-banking Financial Corporation |

BANK |

|

Act of Regulation |

Companies Act, 2013 |

Banking Regulation Act of 1949 |

|

Demand Deposits |

Demand Deposits are not Acceptable |

Can accept demand deposit |

|

Drawing a Cheque |

The cheque cannot be drawn by itself |

You can draw and issue a cheque |

|

Deposit Insurance Facility |

This facility does not accept NBFC deposits |

The facility is open to all bank depositors |

|

Asset restructuring |

|

No Entry |

|

Maintaining Reserve Ratios |

No Mandatory |

The reserve ratio must be maintained |

|

Loan sanction |

Faster and easier |

Comparatively rigid |

|

Product Offering |

Most Property Loans |

There are many types of loans |

|

Foreign Direct Investment (FDI) |

Allowable up to a limit |

Permissible |

|

Statutory Reserve Ratio |

The 15% SLR is a must for deposit-taking NBFCs |

Maintaining SLR as a requirement |

NBFCs are Driving India's Financial Landscape

Below are some specific roles and functions that NBFCs in India perform:

- Transforming Transport & Infrastructure

- Employment Generation

- Increase your wealth.

- Support for improving the financial situation of those in need

- Broad Base Economic Development

- Develop the financial market with flexibility

- Contribution to the State Exchequer of a large amount

- NBFC facilitates long-term audit and Specialized Credit

What are the Documents Required for NBFC Registration?

- Both the company brochure and its management system provide detailed information.

- The CIN (Corporate Identification Number) or PAN (Personal Identification Number) of the applicant

- Documents proving the address and location of the applicant company.

- Certified copy of the MOA (Memorandum of Association), and AOA (Article of Association).

- Each Director must sign the list of directors.

- The Director's CIBIL score or credit report must be submitted.

- The board resolution stating the company does not provide financial services, and will not do so until it is registered as an NBFC.

- Certificate stating that the company does not hold any public deposit issued by the authority concerned and is also not accepting it.

- The company's board resolution demonstrates that the company has complied with the Fair Practices Code in its business activities.

- Document proving the company's Net Owned Fund (NOF) or net owned fund.

- Other details about the company must be provided, including bank account, loans, credits balances

- If the company is not eligible for NBFC registration, they must provide the five-year list of financial statements. A balance sheet, a profit and loss statement, and a directors and auditors report.

- Self-certified Bank Statement for Income Tax Return

- A company must submit information about its plans for at least five years.

The RBI Regulations Penalize Non-Compliance

- If an NBFC is operating without a certificate of registration.

- Operating in the Public Interest

- Refusal to pay the deposit

- Continued default by a defaulting NBFC.

- Non-compliance of the RBI's statutory orders.

- Non-compliance of the Company Law Board's statutory orders.

- The RBI has issued directions to auditors.

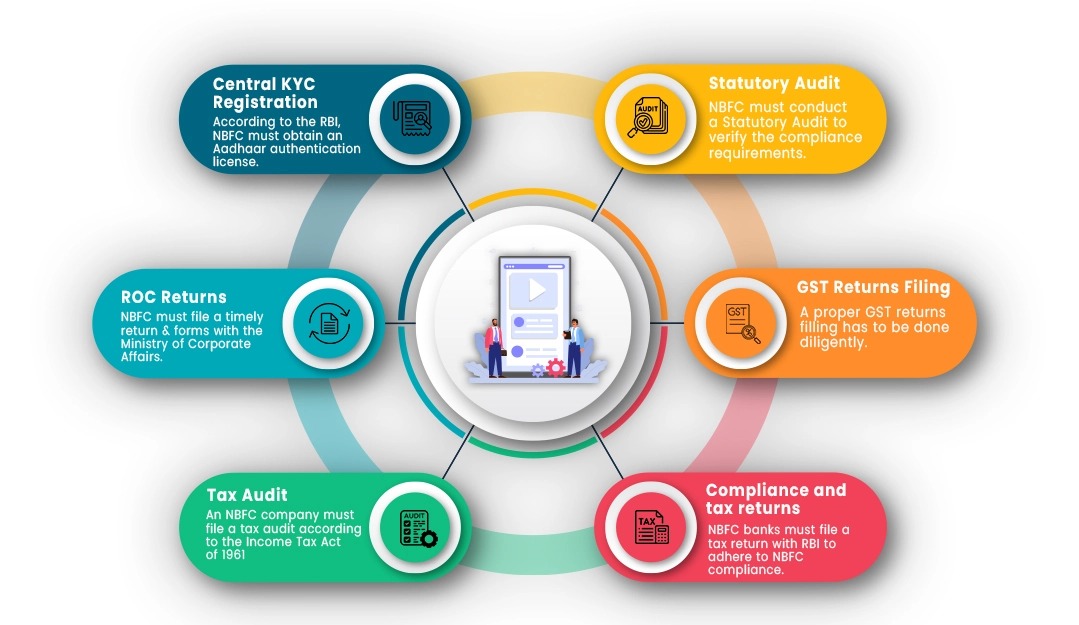

Complainces for an NBFC After Obtaining Registration

What is the NBFC Registration Procedure in India?

- The Companies Act 2013 requires that a company applicant be registered.

- To obtain an NBFC licence, you must have a minimum of 10 crores in net owned funds.

- The applicant must have deposited a fixed deposit of at least Rs. 10 crores in any nationalised bank.

- Foreign Exchange Management is required for all foreign investment applications.

- Applicants must arrange the necessary documents after meeting these requirements.

- The documents must be submitted along with the FD receipt at the Reserve Bank of India or RBI.

- The applicant must also submit an online application through the RBI's official website.

- The applicant company will then need to download the electronic form from the website and submit it electronically.

- In order to track the progress of a request, the applicant must also collect an Application Reference Number (ARN) issued by RBI.

- The applicant should keep a hard copy of the e-form for the reference number.

- The applicant must also submit all necessary documents to the RBI Central Office.

List of RBI Compliance for NBFC

- Fair Practice Code Implementation

- Secretarial compliances

- CIC Registration

- KYC Registration

- COSMOS Registration

- CERSAI Registration

- FIU-IND Registration

- The COSMOS platform is the online platform of RBI.

- Compliance with KYC and Anti-Money Laundering.

NBFC Model Based on FINTECH has many Advantages

The financial industry has evolved with the advent of technology. It is now able to upgrade its business and provide various benefits for the Indian economy. Below are some advantages of Fintech-based NBFC models.

- The advancements in technology have made it easier for customers to solve their problems.

- Online Loan Facility

- Streamlining business operations can increase efficiency.

- Better Risk Management facilities.

- Work on the Financial Inclusion App

Cancellation Request for NBFC Registration

RBI can cancel a NBFC registration application for any of the following reasons.

- Non-maintenance: - When the NBFC fails to meet the minimum requirement of Net Owned Fund (NOF).

- If the NBFC does not operate in the public's interest.

- Failure to Repay Deposits: - NBFC will not repay deposit in accordance with the terms and conditions set forth by the depositor.

- Not operating NBFC activity: - When NBFC does not operate its primary financial business.

- Failure to submit books of accounts: - When the NBFC does not manage its books of account in accordance with RBI guidelines.

- Incorrect profile of Directors: - If the Directors of the applicant fail to meet the criteria according to RBI policies.

- Unsuitable Business Plan: - A business plan of at least five years is required.

- Incorrect profiles of shareholders: – Failure to provide the correct details and identify the shareholders.

FREQUENTLY ASKED QUESTIONS

NBFC stands for Non-Banking Financial Company. It is a type of financial institution that operates without a banking license and provides financial services such as loans, investments, and other financial products and services. It is regulated by the Reserve Bank of India (RBI) and are required to comply with various regulations and guidelines issued by the RBI.

Registering an NBFC in India offers several benefits, including increased credibility and trustworthiness in the eyes of customers and investors, as well as the ability to engage in a wide range of financial activities such as lending, leasing, investment, and insurance. NBFCs can also raise funds and lending capacity through various sources such as fixed deposits, bonds, and commercial papers. Additionally, being an NBFC provides more flexibility, and interest rates can be higher than those offered by banks, leading to increased profit margins. Finally, NBFCs can play a crucial role in promoting financial inclusion by providing loans and other financial services to underserved segments of society, such as low-income households, small businesses, and rural areas.

In India, registration as a Non-Banking Financial Company (NBFC) is open to various entities, including companies registered under the Companies Act of 2013 or its predecessor, the Companies Act of 1956, co-operative societies whose principal business is finance-related activities and registered under any law in force in India, and partnership firms, limited liability partnerships (LLPs), or any other association of persons engaged in the business of providing finance-related activities.

These entities are eligible to apply for registration as NBFCs, subject to compliance with relevant regulations and guidelines laid down by the Reserve Bank of India (RBI).

India has a diverse range of Non-Banking Financial Companies (NBFCs), each with their unique set of rules and regulations. The different types of NBFCs include Asset Finance Companies (AFC), Investment Companies (IC), Loan Companies (LC), Infrastructure Finance Companies (IFC), Systemically Important Core Investment Companies (CIC-ND-SI), Microfinance Institutions (MFI), Non-Banking Financial Companies-Factors (NBFC-Factors), and Non-Banking Financial Companies-Micro Finance Institutions (NBFC-MFIs).

These NBFCs cater to various segments of the economy and offer financial services to individuals and businesses. Each NBFC is regulated by the Reserve Bank of India (RBI) and must adhere to the guidelines and regulations set by the RBI.

An NBFC (Non-Banking Financial Company) is a financial institution that provides financial services like loans, credit facilities, investments, and other financial products, but it cannot accept deposits from the public. In contrast, a bank is a financial institution that accepts deposits from the public and provides a range of financial services. Banks also have additional privileges, such as issuing cheques, providing checking and savings accounts, and providing payment and settlement services. Additionally, banks are more heavily regulated than NBFCs, and are subject to specific regulations under the Banking Regulation Act, 1949.

Non-compliance with NBFC regulations in India can lead to severe consequences, including penalties and legal action by the regulatory authority, the Reserve Bank of India (RBI). The penalties for non-compliance can result in monetary fines, cancellation of registration, and even criminal prosecution. The severity of the violation determines the amount of the penalty, which can range from a few lakh rupees to several crores.

Apart from imposing penalties, the RBI can take additional measures like restricting the NBFC's business operations, removing its directors, or appointing a management team to run the company. Therefore, NBFCs operating in India must comply with the regulatory framework to avoid any adverse actions by the RBI.

Leave a Reply