0% to 9% Corporate Tax in UAE from 1st June 2023: Applicability, Exemptions and Returns

The United Arab Emirates (UAE) issued a corporate tax law that will impose a 9% corporate tax in UAE beginning from 1st June 2023. Corporate taxes are essentially the taxes levied on profits earned by corporate entities. UAE is bringing a series of tax reforms in a bid to diversify its tax revenues and move ahead with international best practices. The UAE corporate tax will be levied on the profits earned by the corporates in UAE. Let’s decode the corporate tax law in UAE, including detailed guidelines and exemptions.

Taxability and Exemption Under UAE Corporate Tax Law 2023

The following person will fall under the corporate tax law in UAE:

- UAE companies and other juridical persons that are either incorporated in UAE or effectively managed and controlled in UAE;

- Individuals who conduct any business activity in UAE. This shall be specified in a cabinet decision in due course;

- Non-resident juridical persons if they have a permanent establishment in UAE.

The law has exempted certain persons from the levy of UAE corporate tax. These include the following:

- Businesses that are registered in Free Trade Zones. However, they should comply with the regulatory requirements and should not be conducting business with Mainland UAE;

- Individuals who are earning income in their personal capacity like investment income, salary income, etc. as long as generating such income does not require a commercial license;

- Entities that are involved in extractive or non-extractive natural resource business if they meet certain conditions. However, the emirate-level taxation will still apply to them;

- Government entities and government-controlled entities;

- Qualifying public benefit entities, if listed in the cabinet decision;

- Public or private social security and pension funds;

- Qualifying investment funds;

- Wholly owned and controlled UAE subsidiaries of the following (if they applied to and are approved by the Federal Tax Authority and meet certain conditions):

- government entities or a government-controlled entity

- public or private social security or pension fund

- qualifying investment fund

Further, the following incomes shall be exempt from corporate tax in UAE:

- Capital gains

- The dividend income that is earned by the UAE companies from their qualifying shareholdings. Qualifying shareholding will be defined by the law.

- Profits from intra-group transactions

- Profits from group reorganization

Further, there will be no withholding taxes in UAE on domestic and cross-border payments.

Corporate Tax Rate in UAE

Following is the corporate tax rate applicable in UAE:

- Resident Taxable Persons

|

Income Criteria |

Tax Rate |

|

Taxable income does not exceed AED 375,000 |

0% |

|

Taxable income exceeds AED 375,000 |

9% |

- Qualifying Free Zone Persons

|

Income Criteria |

Tax Rate |

|

Qualifying income |

0% |

|

Taxable income not meeting the definition of qualifying income |

9% |

How to Pay UAE Corporate Tax?

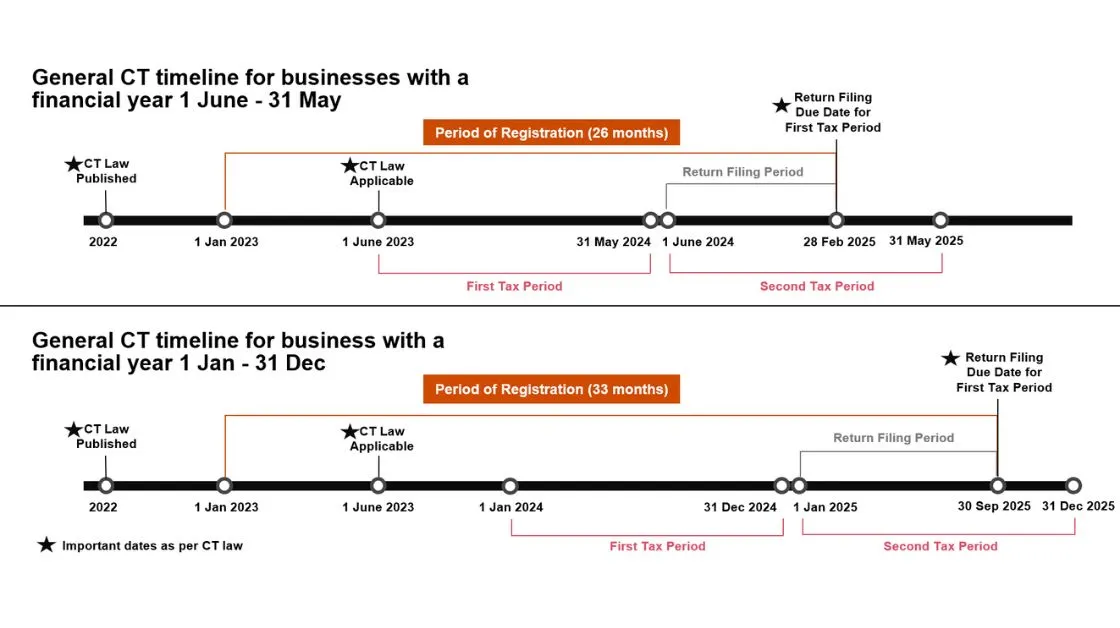

The UAE corporate taxes will be charged on the income earned for the financial year beginning on or after 1st June 2023. All taxable persons, including the free zone persons, shall be required to obtain a Corporate Tax Registration Number in UAE. Such taxable persons shall be required to pay the corporate tax and file a corporate tax return for each tax period within 9 months from the end of the relevant period. However, things will be slightly different for corporates with the financial year from 1st January to 31st December. Let’s have a comparative analysis for both financial years:

|

Particulars |

Financial Year: 1st June 20xx to 31st May 20xx |

Financial Year: 1st January 20xx to 31st December 20xx |

|

Period of registration available |

26 months 1st Jan 2023 – 28th Feb 2025 |

33 months 1st Jan 2023 – 30th Sept 2025 |

|

First Tax Period |

1st June 2023 – 31st May 2024 |

1st Jan 2024 – 31st Dec 2024 |

|

Return filing due date for the first tax period |

28th Feb 2025 |

30th Sept 2025 |

|

Second Tax Period |

1st June 2024 – 31st May 2025 |

1st Jan 2025 – 31st Dec 2025 |

Other Important Provisions for UAE Corporate Taxation

Following are some of the important provisions for UAE corporate taxation:

- Tax losses can be carried forward and set off for an indefinite number of years. Such losses can be set off up to 75% of the taxable income of the concerned year in which such loss shall be set off.

- In case more than 50% of the shareholding has changed, then the tax losses cannot be carried forward unless the same or similar business is carried out.

- The UAE corporate tax law has also introduced anti-abuse rules. This will curb tax avoidance practices. As per these rules, certain transactions entered without any valid commercial reason can be disregarded and bought into the ambit of tax if they were entered only to obtain a tax advantage.

- Group companies in UAE shall be allowed to form a tax group to make a single tax payment and file a single tax return. However, it is subject to the condition that the parent company is holding 95% voting rights, ownership, and rights to the assets and profits of group companies.

What You Should Do?

If you have any permanent establishment in UAE or have incorporated a company in UAE, then you are most likely to fall under the UAE corporate tax. In such case, you need to ask the following questions:

- Whether your business needs to register for corporate tax in UAE and obtain a corporate tax registration number in UAE?

- What will be the tax period for your business?

- What is the due date applicable for filing the UAE corporate tax return of your business?

- What are the various elections and options available under the corporate tax law?

- What are the financial and other records you need to maintain under the corporate tax law?

It would be wiser to contact tax professionals with relevant knowledge and expertise in international taxation matters. They can help guide you through the new UAE corporate tax regime. If you want any assistance regarding UAE corporate tax law, feel free to contact the ASC Group.

Leave a Reply