Political Donations u/s 80GGC – Can Deduction be Denied Merely on Suspicion?

- The increased scrutiny by the Income Tax Department on deductions claimed by the Assessee’s u/s 80GGC of the Income Tax Act, 1961 has opened a new chapter in Tax Litigation i.e. over the last few years, the Investigation Wing has unearthed several instances where certain political parties, were allegedly engaged in providing accommodation entries in the guise of Political Donations. Consequently, thousands of taxpayers across the country have received Notices from the Tax Authorities proposing the disallowance of deduction claimed u/s 80GGC.

- However, an equally important judicial trend has also emerged wherein the Hon’ble Courts and Tribunals have repeatedly held that merely because the recipient political party is found suspicious or involved in dubious activities, the deduction cannot automatically be denied to the assessee unless there exists cogent and substantial evidence directly linking the assessee with the alleged bogus arrangement.

Statutory Framework & requirements for Claiming deduction u/s 80GGC.

- Section 80GGC allows deduction to Assessee in respect of contributions made to Political Party or electoral trust on fulfilment of certain conditions-

- Contribution should not be made in Cash.

- Payment must be through Banking Channels.

- Political party must be registered under Section 29A of the Representation of the People Act, 1951.

- Proper documentary evidence should exist.

The legislative intent behind the provision was to encourage transparency in political funding through traceable Banking mechanisms. However, misuse by certain individuals/entities have now led to departmental Investigations.

- Further, the deduction u/s 80GGC is not available under the New Tax Regime under Section 115BAC and, the said deduction, can effectively be claimed only if the assessee opts for the Old Tax Regime and furnishes the relevant information pertaining to Donations made.

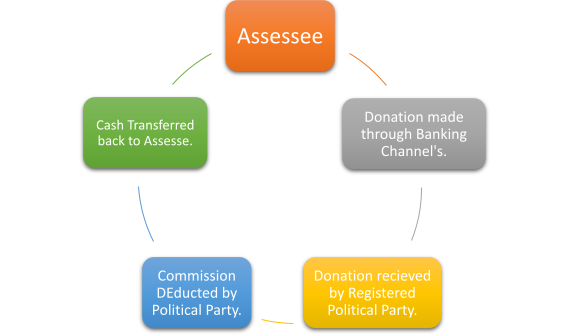

Departmental Allegation - “Bogus Political Donation Scheme”

- The common allegation raised by the Department in such matters is that certain political parties accepted donations through banking channels and thereafter returned the amount in cash to the donor after deducting commission. Based on search and survey proceedings conducted on such Political Parties, the Department often initiates proceedings against donors and, thus, disallows the deduction claimed u/s 80GGC.

- The reliance by the Ld. Assessing Officer in such type of Proceedings are majorly placed upon Third-party statements, Investigation reports; Search findings on political parties, General modus operandi reports, Human probability theory. However, even though the Income Tax Department places its reliance on the same yet the Critical Legal issue still stands i.e.

Can deduction be denied merely because the recipient political party is allegedly tainted, without any direct evidence against the assessee?

Judicial Principle (Suspicion Cannot Replace Evidence)

- The settled principle of law remains that suspicion, however strong, cannot substitute legal proof i.e. unless the Department establishes a direct nexus between the Assessee and the alleged accommodation entry arrangement, deduction cannot be disallowed merely on presumptions.

- The Hon’ble Supreme Court in its decade old Judgement passed in 1959 titled Umacharan Shaw & Bros. Vs. Commissioner of Income-tax [1959] 37 ITR 271 (SC) had evidently laid down the Law that – “There were many surmises and conjectures, and the conclusion was the result of suspicion which could not take the place of proof”.

The said Law has been followed throughout every Hon’ble adjudicating authorities and even the Hon’ble Apex Court have time and again repeated that mere “Suspicion Cannot Replace Evidence”.

- The Hon’ble Tax Tribunals while adjudicating the issue of Donation’s made u/s 80GGC to the Tainted Political Parties have also applied the Law laid down by the Hon’ble Supreme Court and, have thus held that –

|

Hon’ble ITAT, Rajkot Bench Chirag Bhikhabhai Patel Vs. DCIT “There is no single piece of evidence against the assessee despite of this the addition was made by the A.O, only on the basis of assumption.” |

Hon’ble ITAT, Raipur Bench ACIT Vs. Anuj Prakash Gupta “The A.O had not brought out any evidence which suggests that the said political party has derived commission and has paid money back to the assessee through backdoor.” |

Conclusion

- Recent wave of Litigation concerning bogus donations u/s 80GGC highlights an important balance between Tax enforcement and Taxpayer rights.

- The Department is justified in investigating Tax Evasion involving sham political contributions. However, law equally mandates that additions and disallowances must rest upon credible evidence and not mere suspicion.

- The judicial consensus on this topic has been clear that –

“A political party may be tainted, but unless the assessee is proven to be involved the deduction u/s 80GGC cannot be denied solely on general investigation findings.”

In view of the above, while bogus claims deserve strict action, genuine Taxpayers cannot be penalized merely because the recipient entity subsequently becomes subject matter of departmental investigation.

Leave a Reply