Amendment in Form 48, Form 3CEB, Form ITR-6 and Introduction of new rules

Introduction to Form 3CEB and Transfer Pricing

Transfer Pricing (TP) governs how transactions between related parties - formally called Associated Enterprises (AEs) - are priced to ensure fairness and prevent profit shifting across borders. In India, the Income Tax Act, 1961 mandated that taxpayers with international transactions report those transactions in Form 3CEB, certified by a Chartered Accountant. This form has been the cornerstone of India's Transfer Pricing Audit framework for over two decades.

With the introduction of the Income Tax Act, 2025, this landscape is undergoing a significant transformation. Form 3CEB is expected to be replaced by Form 48, which introduces enhanced disclosure requirements aligned with global BEPS (Base Erosion and Profit Shifting) standards and modern MNC reporting norms.

What Is an Associated Enterprise (AE)?

Under Section 92A of the Income Tax Act, 1961 (and the corresponding provisions of the Income Tax Act, 2025), an enterprise is considered an AE if it holds at least 26% voting power in another enterprise, or exercises management control, directly or indirectly. Transactions between AEs - whether involving goods, services, royalties, loans, or intangibles - are subject to TP regulations and must be reported at arm's length.

Applicability of Form 3CEB

Form 3CEB applies to any Indian taxpayer who has entered into international transactions with an AE where the aggregate value exceeds Rs. 1 crore, or specified domestic transactions exceeding Rs. 20 crore. The form must be certified by an independent Chartered Accountant and filed along with the income tax return.

Transfer Pricing Methods

The Income Tax Act prescribes six approved methods for determining the arm's length price of an international transaction: Comparable Uncontrolled Price (CUP), Resale Price Method (RPM), Cost Plus Method (CPM), Profit Split Method (PSM), Transactional Net Margin Method (TNMM), and any other method notified by the CBDT. TNMM remains the most widely used method in practice due to its flexibility.

Due Dates and Penalties

The due date for filing Form 3CEB (and, going forward, Form 48) is October 31 of the relevant assessment year, for taxpayers whose accounts are required to be audited. Failure to furnish the form attracts a penalty of 2% of the value of the international transaction under Section 271BA, and concealment of income related to TP adjustments can attract penalties up to 300% of the tax evaded.

What's New: Form 48 Under the Income Tax Act, 2025

Key update: The Income Tax Act, 2025 proposes to replace Form 3CEB with Form 48, introducing expanded disclosure requirements for international transactions, specified domestic transactions, and intra-group services.

Form 48 is designed to capture a broader set of information, including country-by-country reporting linkages, digital economy transactions, and disclosures related to intangibles and financial arrangements. It also requires taxpayers to confirm compliance with OECD Transfer Pricing Guidelines, bringing Indian norms closer to international standards.

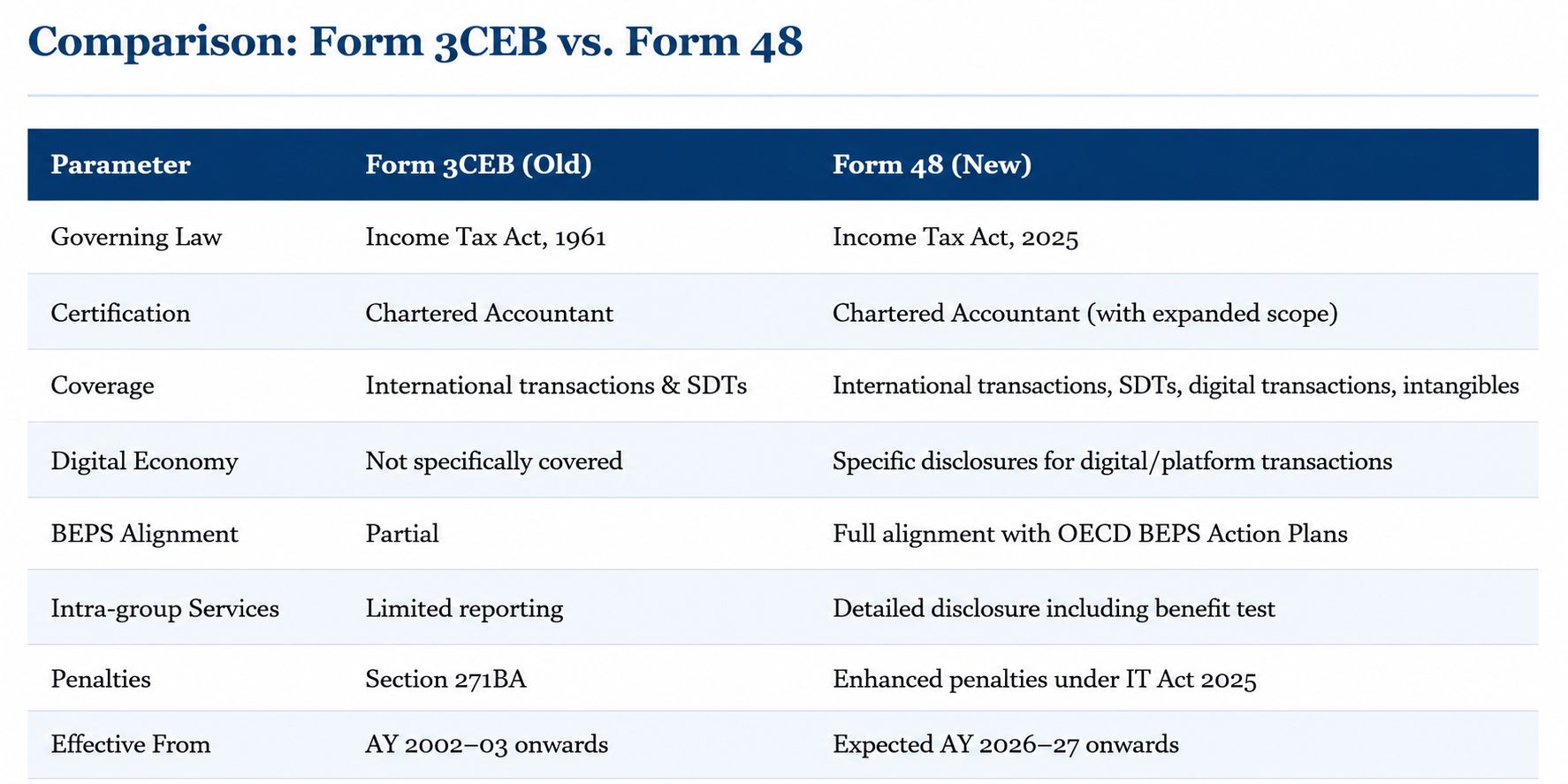

Comparison: Form 3CEB vs. Form 48

Transition Phase: What Happens Now?

The Income Tax Act, 2025 is expected to come into full force from Assessment Year 2026–27. During the transition, taxpayers should continue filing Form 3CEB where applicable, while preparing their documentation frameworks to comply with the expanded requirements of Form 48. The CBDT is expected to issue detailed rules and a prescribed format for Form 48 before the Act takes effect.

Impact on Key Business Segments

MNCs and Foreign Subsidiaries

Multinational corporations with Indian subsidiaries will need to update their intercompany agreements, benchmarking studies, and master file disclosures to align with Form 48 requirements.

IT/ITES and Export-Driven Companies

IT and ITES companies, which rely heavily on cost-plus or TNMM arrangements, will face heightened scrutiny on profit margins and benefit tests for intra-group services.

Startups with Foreign Investment

Startups receiving funding from foreign AEs or licensing IP to group entities will need to carefully document their TP policies, as Form 48 requires more granular disclosure of intangible-related transactions.

Earlier Amendment: CBDT Notification 82/2020

As a point of historical reference, CBDT Notification 82/2020 (effective 01.10.2020) amended Form 3CEB to require reporting of transactions with persons who had opted for the concessional tax regime under Section 115BAB - specifically where such transactions resulted in more than ordinary profits. This amendment, alongside changes to Form 3CD and ITR-6, reflected CBDT's effort to prevent profit-shifting into tax-preferred entities. These reporting requirements remain in force until Form 48 is formally notified.

Required Documents for Transfer Pricing Compliance

Taxpayers should maintain contemporaneous documentation including: a functional analysis of the transaction, benchmarking study with comparable data, intercompany agreements, economic analysis justifying the chosen TP method, and master file/local file documentation where CbCR thresholds apply.

FAQs: Form 3CEB and Form 48

Q1. Is Form 3CEB still applicable for AY 2025–26?

Yes. Form 3CEB continues to apply for AY 2025–26. Form 48 is expected to replace it from AY 2026–27, subject to CBDT notification of the prescribed format.

Q2. What is the threshold for filing Form 3CEB / Form 48?

International transactions with AEs aggregating more than Rs. 1 crore, or specified domestic transactions exceeding Rs. 20 crore, require TP certification.

Q3. Does Form 48 change the Transfer Pricing methods available?

No. The six prescribed methods remain unchanged. However, Form 48 requires additional justification for the selected method and expanded benchmarking disclosures.

Q4. Will startups be exempt from Form 48 requirements?

No general exemption is proposed. Startups with AE transactions above the threshold will be subject to Form 48, with particular focus on IP and funding arrangements.

Q5. What should businesses do now to prepare for Form 48?

Businesses should review their intercompany agreements, update TP documentation policies, and engage their tax advisors to gap-assess current practices against the expanded disclosures expected under Form 48.

Conclusion: What Businesses Should Do Now

The shift from Form 3CEB to Form 48 under the Income Tax Act, 2025 is not merely administrative — it represents a fundamental upgrade to India's Transfer Pricing compliance architecture. Businesses should use this transition period to audit their existing TP documentation, revisit intercompany pricing policies, and align with OECD standards. Those who prepare proactively will be far better positioned for Transfer Pricing Audits under the new regime. Engaging a qualified transfer pricing specialist now, rather than at the filing stage, is the most prudent course of action.

Leave a Reply